Can I Reaffirm A Credit Card In Chapter 7

Can I Reaffirm A Credit Card In Chapter 7 - “reaffirmation” refers to the process whereby a debtor agrees to (re)payment terms with the creditor on a debt instead of having it discharged in the. Web chapter 7 debtors must file a statement of intention within 30 days of the petition date or the date of the 341 meeting, whichever is earlier. If you don't reaffirm, the worst thing a creditor can do. Here are some important steps to begin rebuilding your credit after bankruptcy. They come in handy when you want to keep a specific asset while filing for a chapter 7 bankruptcy. Web if you’re in chapter 7 bankruptcy and want to renegotiate the terms of your car loan, entering into a reaffirmation agreement with your lender might be the answer. Web in addition, no individual may be a debtor under chapter 7 or any chapter of the bankruptcy code unless he or she has, within 180 days before filing, received credit counseling from an approved credit. You would owe that single debt as if you hadn’t filed the chapter 7. Web reaffirmation agreements are a special feature of chapter 7 bankruptcy. You are not required to reaffirm any debt or sign any agreement regarding a debt that has been or will be discharged in your bankruptcy case.

They come in handy when you want to keep a specific asset while filing for a chapter 7 bankruptcy. Web it is possible to reaffirm credit card debt in a chapter 7 bankruptcy. Web when you reaffirm a debt in chapter 7 bankruptcy, you enter into a contract with your lender (called a reaffirmation agreement) that makes you personally liable for the obligation despite your bankruptcy. If you file for chapter 7, the creditor can… The main consequence of a reaffirmation agreement is that it excludes that particular debt from the discharge of your debts. Web in addition, no individual may be a debtor under chapter 7 or any chapter of the bankruptcy code unless he or she has, within 180 days before filing, received credit counseling from an approved credit. You'll also learn how to qualify for a chapter 7 credit card discharge and whether credit card balances get paid in chapter 7. Web what is the difference between reaffirming a credit card debt vs not including the debt in chap 7 bankruptcy. Web chapter 7 debtors must file a statement of intention within 30 days of the petition date or the date of the 341 meeting, whichever is earlier. However, keep in mind that while chapter 7 offers many benefits, it might not be the best bankruptcy chapter.

If you don't reaffirm, the worst thing a creditor can do. [1] they must perform their stated intention within 30 days of the. Grounds for denial of a debt discharge. Web when you reaffirm a debt in chapter 7 bankruptcy, you enter into a contract with your lender (called a reaffirmation agreement) that makes you personally liable for the obligation despite your bankruptcy. Web a reaffirmation agreement is an agreement that chapter 7 debtors may sign to reassume personal liability for secured debt and keep the collateral. Web that usually happens about 60 days after your “meeting of creditors,” or about 3 months after your chapter 7 filing. Web unsecured credit card debt in chapter 7. Web when you can get a credit card after chapter 7. However, keep in mind that while chapter 7 offers many benefits, it might not be the best bankruptcy chapter. The grounds for denying an individual debtor a discharge in a chapter 7.

Teamsters and IATSE Reaffirm 'Mutual Aid and Assistance Pact

If you don't reaffirm, the worst thing a creditor can do. That's because most of your accounts are likely unsecured. They give your creditors a chance to get you back on the hook for debt you would have otherwise discharged in the bankruptcy by allowing you to reaffirm… The main consequence of a reaffirmation agreement is that it excludes that.

Agusto, GCR Reaffirm ‘AAA’ Rating, Stable Outlook Of Infracredit

Web unsecured credit card debt in chapter 7. You'll also learn how to qualify for a chapter 7 credit card discharge and whether credit card balances get paid in chapter 7. Of course getting a credit card soon after bankruptcy. That's because most of your accounts are likely unsecured. You are not required to reaffirm any debt or sign any.

ionic 5 tutorials how to create ionic card ionic 5 card chapter 7

You'll also learn how to qualify for a chapter 7 credit card discharge and whether credit card balances get paid in chapter 7. Web chapter 7 debtors must file a statement of intention within 30 days of the petition date or the date of the 341 meeting, whichever is earlier. Web a chapter 13 bankruptcy, which restructures your debts so.

Lecture 13Credit Cards (Chapter 6) YouTube

Web when you can get a credit card after chapter 7. [1] they must perform their stated intention within 30 days of the. Web reaffirmation agreements are a special feature of chapter 7 bankruptcy. Web what is the difference between reaffirming a credit card debt vs not including the debt in chap 7 bankruptcy. Grounds for denial of a debt.

SHOULD I REAFFIRM MY MORTGAGE AGREEMENT AFTER MY CHAPTER 7 BANKRUPTCY?

That's because most of your accounts are likely unsecured. Web if you’re in chapter 7 bankruptcy and want to renegotiate the terms of your car loan, entering into a reaffirmation agreement with your lender might be the answer. Of course getting a credit card soon after bankruptcy. Web regardless of the reason a debtor chooses to reaffirm, their decision is.

Bankruptcy 101 LoanPro Help

Web reaffirmation agreements are a special feature of chapter 7 bankruptcy. “reaffirmation” refers to the process whereby a debtor agrees to (re)payment terms with the creditor on a debt instead of having it discharged in the. However, keep in mind that while chapter 7 offers many benefits, it might not be the best bankruptcy chapter. Types of credit cards you.

Reaffirm Your Faith in Him iDisciple

Web certain debts can not be discharged in a chapter 7 or a chapter 13 bankruptcy case. Web chapter 7 debtors must file a statement of intention within 30 days of the petition date or the date of the 341 meeting, whichever is earlier. Web reaffirming protects against the possibility of getting your property repossessed when you are still making.

6 Things You Can Reaffirm for Positive Change and Validation

The balance on the majority of the cards in your wallet will get wiped out in chapter 7 bankruptcy. Web for instance, if you received a discharge in a chapter 7 case, you can’t receive another chapter 7 discharge for eight years. Web if you want to keep your financed car in chapter 7 bankruptcy, your lender might require you.

Nudgee Stakes Kisukano can reaffirm her reputation as one of

Im employed by the dept store that issued the charge, therefore i would like to keep the charge. You would owe that single debt as if you hadn’t filed the chapter 7. Web what is the difference between reaffirming a credit card debt vs not including the debt in chap 7 bankruptcy. The main consequence of a reaffirmation agreement is.

REAFFIRM Synonyms and Related Words. What is Another Word for REAFFIRM

That's because most of your accounts are likely unsecured. Web when you reaffirm a debt in chapter 7 bankruptcy, you enter into a contract with your lender (called a reaffirmation agreement) that makes you personally liable for the obligation despite your bankruptcy. A reaffirmation agreement is a. Why you may not wish to reaffirm. Web the credit card company knows.

Web What Is The Difference Between Reaffirming A Credit Card Debt Vs Not Including The Debt In Chap 7 Bankruptcy.

Web certain debts can not be discharged in a chapter 7 or a chapter 13 bankruptcy case. Here are some important steps to begin rebuilding your credit after bankruptcy. Types of credit cards you can qualify for after filing chapter 7 bankruptcy credit cards that you might qualify for may be secured or unsecured. You are not required to reaffirm any debt or sign any agreement regarding a debt that has been or will be discharged in your bankruptcy case.

Web For Instance, If You Received A Discharge In A Chapter 7 Case, You Can’t Receive Another Chapter 7 Discharge For Eight Years.

You'll also learn how to qualify for a chapter 7 credit card discharge and whether credit card balances get paid in chapter 7. You would owe that single debt as if you hadn’t filed the chapter 7. Web reaffirming protects against the possibility of getting your property repossessed when you are still making timely payments. Web if you’re in chapter 7 bankruptcy and want to renegotiate the terms of your car loan, entering into a reaffirmation agreement with your lender might be the answer.

Why You May Not Wish To Reaffirm.

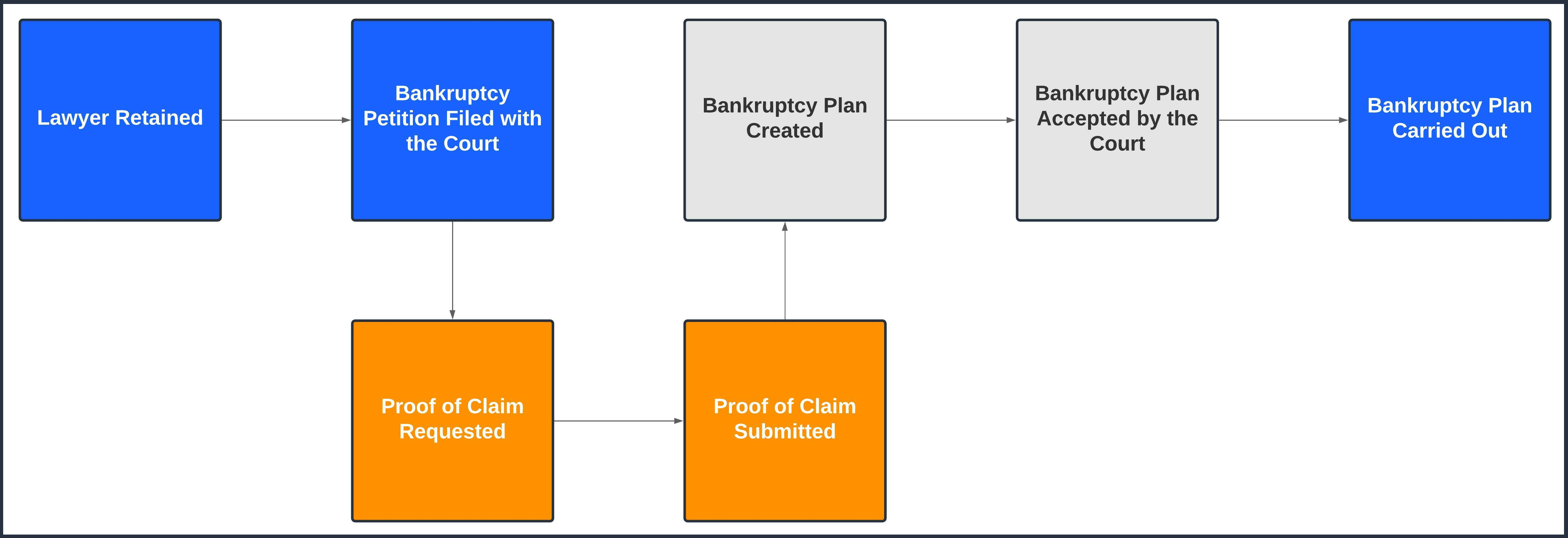

Web a reaffirmation agreement is an agreement that chapter 7 debtors may sign to reassume personal liability for secured debt and keep the collateral. The grounds for denying an individual debtor a discharge in a chapter 7. A reaffirmation agreement is a. Web that usually happens about 60 days after your “meeting of creditors,” or about 3 months after your chapter 7 filing.

Web If You Want To Keep Your Financed Car In Chapter 7 Bankruptcy, Your Lender Might Require You To Enter Into A New Contract In A Process Known As Reaffirming The Debt.

Web regardless of the reason a debtor chooses to reaffirm, their decision is likely to have a quick and positive impact on their credit score, as the creditor will be required to notify the credit bureaus. If you don't reaffirm, the worst thing a creditor can do. Web when you can get a credit card after chapter 7. Web in addition, no individual may be a debtor under chapter 7 or any chapter of the bankruptcy code unless he or she has, within 180 days before filing, received credit counseling from an approved credit.